Enterprise Portfolio Coordination: Built for the Way Portfolios Work Now

One operating layer where investment models, overlay, portfolio-wide intelligence, advisor activity, and compliance finally work together.

The Real Problem: Most UMA and UMH Programs Stop at Registration-Level Unification

The systems managing sleeves, overlay, taxes, compliance, advisor activity, and execution often remain disconnected beneath the surface.

Modern portfolio construction has evolved dramatically over the last decade. The infrastructure supporting it largely hasn’t.

Enterprise RIAs are managing increasingly sophisticated household structures that combine direct indexing, SMA sleeves, alternatives, ETFs, and advisor-built models across multiple custodians. Broker-dealers are trying to balance advisor flexibility with centralized oversight, pre-trade supervision, and platform-wide consistency.

On paper, both models appear operationally mature.

Underneath, many firms are still coordinating portfolios through disconnected systems that were never designed to operate together in real time. That disconnect is the real problem most portfolio infrastructure conversations fail to address.

Unified Managed Account environments are unified at the registration level only. The client sees one account. The statement shows one portfolio. Reporting appears consolidated.

But beneath the surface, the systems responsible for sleeves, overlay management, tax optimization, compliance, execution, and platform-wide operational visibility often operate independently of one another.

The result is operational fragmentation hidden beneath an attempt to deliver a unified client experience.

On a smaller scale, firms can work around these gaps manually. Advisors know their accounts or households personally. Operations teams compensate for disconnected systems through spreadsheets, tribal knowledge, and repetitive reconciliation processes.

As firms grow, those operational workarounds begin compounding quickly.

One system may manage portfolio strategies. Another handles execution. Overlay logic lives elsewhere. Compliance validates activity after the fact. Tax optimization only sees part of the portfolio structure. Advisor activity may operate independently from the home-office visibility layer.

Everything technically exists within the same environment, but the workflow underneath the portfolio remains fragmented.

Connection Where There Is Fragmentation

Your UMA isn’t unified. It’s stitched together.

Most firms assume a UMA means everything is operating in one place. In reality, many firms are simply consolidating reporting while the operational workflows underneath remain disconnected.

A portfolio may appear coordinated because sleeves sit under one registration and the client receives one consolidated statement. But operationally, execution context remains fragmented, tax decisions happen sleeve by sleeve, oversight lives outside the workflow, and portfolio visibility is incomplete.

The moment a model is created in one system, executed somewhere else, and monitored in another environment, drift begins to emerge across the operating model.

That drift may not be immediately visible.

In many cases, the portfolio still appears functional on the surface. But underneath, firms begin accumulating operational inefficiencies that become harder to manage as complexity grows.

Tax optimization decisions conflict with portfolio exposures. Overlay decisions lose full portfolio context. Compliance visibility arrives after implementation. Execution behavior becomes inconsistent across advisors and custodians.

Growth will eventually expose this problem.

Why Modern UMH Complexity Is Different

Unified Managed Households structures were originally designed around simpler portfolio models, but today’s environments look very different.

A single household may combine:

- direct indexing

- concentrated stock positions

- active SMA managers

- advisor customization

- ETF allocations

- multi-custodial relationships

- alternatives

Each additional layer increases operational coordination requirements.

The challenge is no longer simply supporting more products or more customization.

Modern firms already have those capabilities.

The challenge is coordinating all of it operationally without creating exponential complexity underneath the surface.

That is where most UMH environments begin to break down.

How Fragmentation Shows Up for Enterprise RIAs

Enterprise RIAs often experience fragmentation when household-level tax management, overlay coordination, execution, and portfolio visibility operate across disconnected systems.

A single client relationship may involve taxable accounts, retirement assets, trusts, direct indexing sleeves, and advisor-managed allocations spread across multiple custodians.

The portfolio strategy itself may be sophisticated and highly customized. The challenge is coordinating all of it operationally in real time. This is where many firms begin losing efficiency without realizing it.

Tax-loss harvesting may optimize one sleeve while creating unintended consequences elsewhere in the household. Asset-location decisions may ignore multi-custodial portfolio structures. Overlay logic may evaluate accounts independently rather than coordinating decisions household-wide.

Advisors may believe they are managing one cohesive financial structure while the underlying systems continue operating through fragmented pools of information.

The client experiences one household.

Most systems still see disconnected accounts.

That disconnect creates operational leakage across the entire portfolio lifecycle.

How Fragmentation Shows Up for Broker-Dealers

For broker-dealers, the fragmentation tends to surface through governance, supervision, and platform visibility.

Many firms support advisor environments where advisors maintain flexibility to customize models, build sleeves if that’s even an option, and manage implementation decisions independently. But the workflows supporting those decisions often remain disconnected from execution oversight and supervision infrastructure.

An advisor may build a model in one system, execute trades somewhere else, trigger suitability checks in another environment, and generate compliance review after execution has already occurred.

Meanwhile, the home office operates from snapshots rather than live operational visibility.

The platform may appear coordinated organizationally.

Operationally, supervision is often reactive.

This creates a difficult balancing act for broker-dealers trying to preserve advisor flexibility while maintaining consistent governance standards across the platform.

Oversight either slows advisors down or arrives too late to prevent operational risk from accumulating underneath the surface.

That tension is not fundamentally a compliance problem.

It is an infrastructure coordination problem.

What a Unified Managed Account Is Supposed to Do

A Unified Managed Account (UMA) is a single account structure that combines multiple investment strategies under one coordinated overlay framework. A Unified Managed Household (UMH) aggregates individual accounts to promote unified management of assets across accounts and sleeves.

At its best, a UMH should function as a coordinated operating model rather than simply a consolidated registration structure.

Multiple sleeves, strategies, managers, custodians, and household accounts should behave as one connected portfolio system. Overlay management, tax awareness, execution, compliance, and reporting should operate from shared context rather than isolated workflows.

That is the promise most firms are actually trying to achieve.

The goal is not simply placing multiple strategies inside one account.

The goal is making those strategies coordinate operationally as one portfolio.

Most UMA platforms still stop short of that.

Why Most UMH Platforms Still Feel Fragmented

Some UMH platforms coordinate account registration, but not the full operating model underneath the portfolio.

Firms still rely on one system for sleeves, another for execution, another for overlay management, another for compliance, and another for reconciliation. Spreadsheets continue bridging the operational gaps between them.

Each system performs its own function reasonably well.

The problem is that none of them share a unified operational context.

That fragmentation creates delayed oversight, duplicated operational work, inconsistent execution behavior, and tax inefficiencies that compound as portfolios become more sophisticated.

This is why many firms still experience operational friction even after modernizing portions of the stack.

The tools may be newer.

The workflow underneath them often remains unchanged.

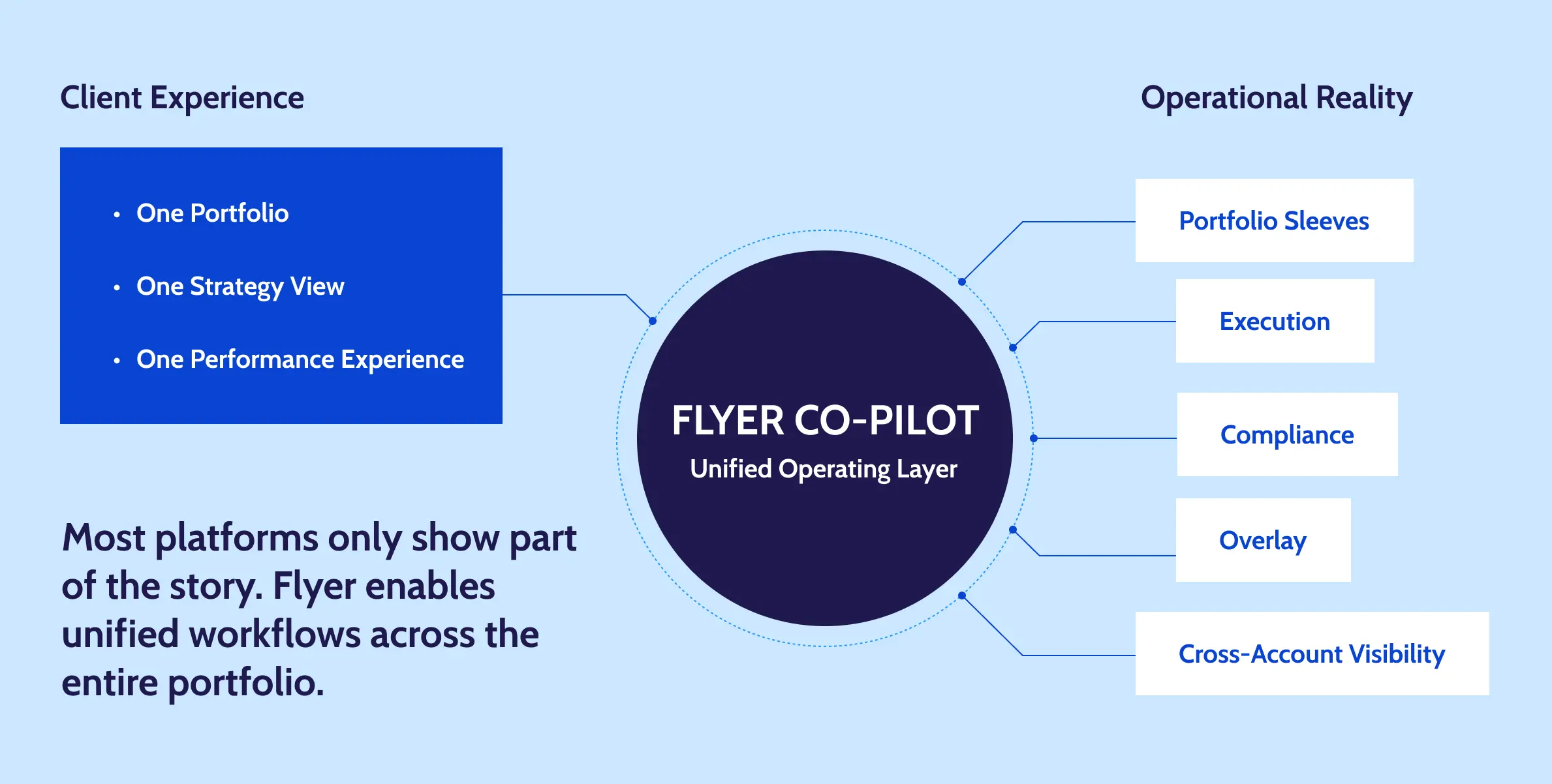

The Missing Layer

This isn’t another system. It’s the layer everything else relies on.

Most firms already have portfolio tools, execution systems, compliance frameworks, proposal systems, and overlay engines.

What they usually do not have is the infrastructure layer connecting them together.

Without that layer:

- workflows fragment

- execution loses context

- oversight becomes reactive

- operational complexity compounds

Firms begin hiring around the fragmentation instead of solving it structurally.

That works temporarily.

It does not scale.

What Flyer Becomes

Flyer is the operating layer connecting portfolio construction, execution, compliance, and oversight into one coordinated system.

For ERIAs, Flyer creates one source of truth across custodians while coordinating household-aware tax decisions, overlay management, and execution workflows from a shared operational context.

For IBDs, Flyer embeds oversight directly into advisor workflows while connecting advisor activity, supervision, execution, and compliance into one coordinated operating environment.

This is the difference between:

- a collection of disconnected systems

- and a coordinated operating model

FAQ: Unified Managed Accounts, Overlay, and Advisor

What is a Unified Managed Account (UMA)?

A Unified Managed Account (UMA) is a single managed account structure that combines multiple investment strategies under one coordinated overlay framework. A UMA may include SMA sleeves, ETFs, direct indexing strategies, alternatives, and advisor-managed allocations operating together inside one portfolio structure.

What is a Unified Managed Household (UMH)?

A Unified Managed Household is a holistic portfolio management framework that treats every member of a client’s household as a single, coordinated investment entity — allowing advisors to optimize assets, tax exposure, and risk across all accounts, vehicles, and generations under one unified strategy.

What is the difference between a UMA and an SMA?

An SMA typically represents one manager or one investment strategy inside a dedicated account. A UMA coordinates multiple sleeves, managers, and strategies together under one account, overlay and reporting structure.

What is overlay management in a UMA or UMH?

Overlay management coordinates tax optimization, drift management, compliance rules, rebalancing, and risk controls across all sleeves inside the portfolio or household. The overlay layer is what allows multiple strategies to behave like one coordinated portfolio system.

Why do many UMA and UMH platforms still feel fragmented?

Many UMA and UMH environments still rely on disconnected systems for execution, compliance, overlay management, household visibility, and reporting. While reporting may appear unified, the operational workflows underneath the portfolios often remain disconnected.

How are Unified Managed Household portfolios managed?

Household-level portfolio management evaluates taxes, risk, allocations, and exposures across all accounts within a client household rather than optimizing each account independently.

Why is household visibility important in a UMA?

Without household-level visibility, firms may unintentionally create wash sales, duplicate exposures, asset-location conflicts, and inconsistent tax decisions across accounts.

What is advisor?

Advisor refers to advisor-managed portfolio models where broker dealer financial advisors maintain discretion over portfolio construction and implementation decisions within client agreed to and firm-defined governance structures.

Why is advisor difficult to scale?

Advisor environments become difficult to scale when advisor activity, execution, supervision, and compliance operate through disconnected systems. This often creates less than ideal client outcomes, delayed oversight and inconsistent governance visibility across the platform.

What causes operational drift inside a UMA or program?

Operational drift usually emerges when portfolio construction, execution, tax management, compliance, and oversight operate independently from one another without shared operational context.

What does Flyer Co-Pilot do?

Flyer Co-Pilot operates as the infrastructure layer connecting portfolio construction, execution, compliance, household intelligence, and oversight into one coordinated operating system.

How does Flyer support Enterprise RIAs?

Flyer helps enterprise RIAs coordinate household-level visibility, overlay management, tax-aware portfolio decisions, execution workflows, and multi-custodial portfolio operations inside one operating environment.

How does Flyer support IBDs?

Flyer helps broker-dealers support Rep-as-PM flexibility while embedding governance, supervision, compliance, and execution oversight directly into advisor workflows.